I grabbed a copy of TD’s 2007 Semi-Annual Financial Report on mutual funds over the weekend and took a glance at the TD Health Sciences Fund (TDB976) for interest’s sake. For those who follow my blog & posts in the online forums, I manage my own portfolio of health related stocks. From time to time I like to see what the “smarter people” are managing to do with everyone else’s money to give me some sense of how my own portfolio stacks up.

YTD the fund is down 4.75% and the track record for the 2.70% MER fund is poor to say the least. As I’ve mentioned before in a previous thread, my feelings about how this category of funds is organized and run is not positive. Although the demographics of the aging population SHOULD translate into one or more successful investment strategies, these funds routinely give the sector a bad image. Like all sectors, there are both good and bad companies to own. The problem with healthcare funds in general is that they own just enough of the good ones and almost all of the bad ones to generate mediocre returns. They suffer from over diversification, which when added to that the exorbitant amount of MER that the manager’s charge you’re left with one demoralizing and frustrating situation as an investor.

When looking at the top 10 holdings of the fund, you’ll quickly notice that they comprise only 25% of the portfolio with a whopping 183 positions in stocks. That’s right folks…almost 200 stocks for a portfolio with only $217M in assets (over-diversification much?)

But examine the breakdown of the fund for yourself. See anything interesting?

When I looked through the books of the fund and the breakdown of what it owns stock in, I noticed a few things that stood out…

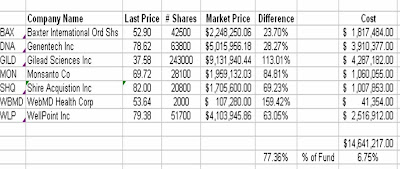

Table 1 shows 7 respective stocks that account for 6.75% of the fund. It’s not a large portion of the fund, but its enough to pay attention towards. The average gain against the cost of those investments (as of Sept 10th) stands at 77% – which many investors would be very happy with if those positions were sold today.

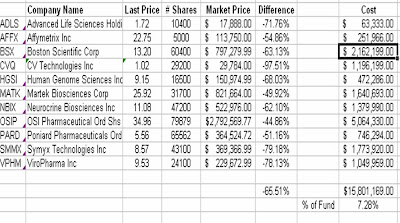

Yet, when you take a look at Table 2 the picture isn’t nearly as rosy. The 11 stocks listed comprise 7.3% of the fund, but the average loss of the group sits at -65.5%. That’s a loss of more than $9.5M…we’re not talking pennies here. None of these companies show promise anytime in the future and its unrealistic at any point to assume that they’ll all appreciate back to the cost of the initial investment in the next year or two (if ever). A properly managed fun would allow a specific MoS in order to help protect the base of assets from significant losses. A manager would sell a position when a specific loss or element of risk emerged in the market with respect to one of these companies. But when TD is generating almost $6M in fee revenues on a yearly basis – they’re unlikely to change their strategy unless unit holders revolt in a serious manner.

Still, it’s important to put this example into context. I’m not suggesting that all stocks held within this group of funds are poor quality investments – simply stating that the structure through which these funds are designed, managed and the high MER defeats the purpose of using it as an investment to diversify an investing strategy into this sector of stocks.